New Section 899 Foreign Provision would have a substantial impact on Foreign Investors and entities involved in U.S. Business.

The House passed their proposal of the tax package as part of the One Big Beautiful Bill Act (“OB3”) on May 22, 2025. This bill delivers on the House promise to be an all-inclusive tax bill, considering both revenue generators and tax cuts. While many of the international tax provisions had minor changes to the current taxing regimes, this OB3 bill introduces a brand new tax provision, Section 899, titled “Enforcement of Remedies Against Unfair Foreign Taxes.”

Section 899 Explained

The new Section 899 provision is intended to target countries that have issued regulations that the House deems to be “unfair,” including new Digital Service Taxes (DSTs) and foreign country minimum taxes introduced within OECD Pillar 2 regulations known as the Undertaxed Profits Rule Taxes (UTPRs). Countries impacted by this regulation would include major U.S. trading partners including Canada, the UK, Brazil, South Korea, India and much of the European Union. While DST and UTPR taxes are issued by foreign governments, the additional taxes under Section 899 would be levied upon individuals and businesses invested or doing business in the U.S.

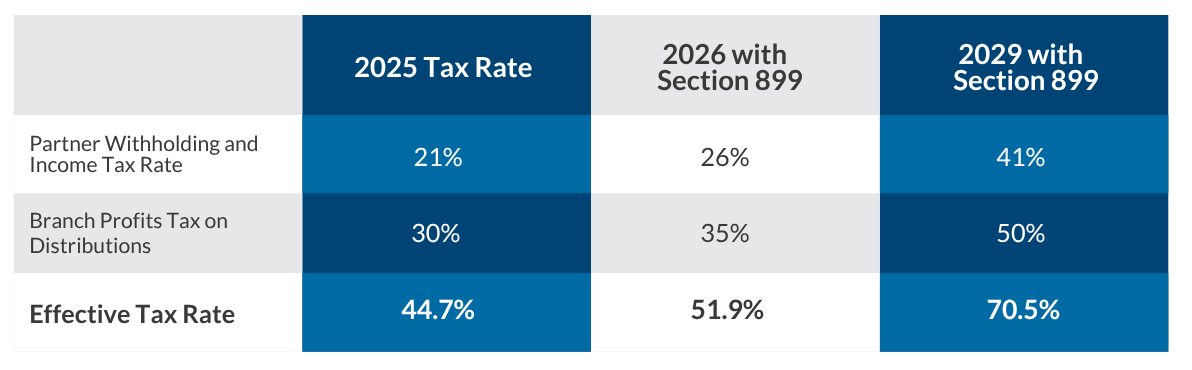

Section 899 would increase the tax rate and withholding tax rate on U.S. source income, overriding pre-established income tax treaty rates. Withholding taxes on cross-border payments to foreign taxpayers in “unfair” taxing jurisdictions would be subject to additional 5% tax rate, increasing annually up to a 20% increase over current withholding tax rates. Non-resident individuals and foreign organizations would similarly see an increase in their income tax rates on U.S.-source income. In addition, corporations subject to the Base Erosion and Anti-Abuse Tax (BEAT) would face an increased BEAT tax rate of 12.5%, up from 10% in 2025.

These additional taxes would continue for any individual or entity residents in countries who continue to impose Digital Service Taxes or Pillar 2 Top-Off taxes without providing a Safe Harbor for U.S. companies.

Background of DSTs and Pillar 2

Digital Service Taxes are a relatively new tax first implemented in France in 2019 and have since been implemented in other European countries. These taxes target revenues generated by large technology companies that provide digital services to foreign companies. DST is generally only applicable to companies with global revenues exceeding €750 million. Due to the controversy that these taxes place a higher burden on U.S. technology companies, there have been efforts through the OECD to establish a global framework to provide a more coordinated approach.

The OECD had also already released coordinated approach to deal with worldwide profit shifting and a continued “race to the bottom” of countries implementing increasingly lower corporate tax rates. Similar to the Global Intangible Low-Taxed Income (GILTI) provisions within the U.S. tax regulations, Pillar 2 aims to establish a global minimum tax rate to ensure that multinational enterprises pay a minimum level of tax to their profits. If profits are undertaxed in a particular jurisdiction, the UTPR allows other jurisdictions to apply additional taxes to profits. Similar to DSTs, this tax would apply only to companies with global revenues exceeding €750 million.

Despite the above taxes only being applicable to large multinational entities, the proposed Section 899 within the One Big Beautiful Bill would apply to all residents with taxable income related to U.S. sources.

Examples of Foreign Persons Impacted by Section 899

A Canadian resident receives a dividend from a U.S. corporation of which it has a 20% ownership. Withholding tax is deducted from the payment of the dividend prior to final net cash payment to the Canadian individual.

A Brazilian company is a partner in a U.S. partnership and receives a K-1 for its portion of U.S. profits. The Brazilian entities files in the U.S. to report its U.S. income and appropriately pay the related U.S. income tax.

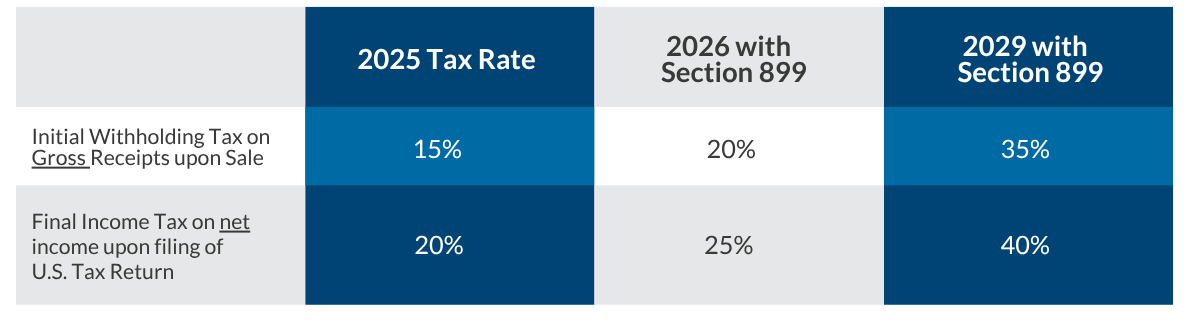

A French real estate investor owns a rental property in Florida for several years. They sell their rental property to a U.S. person. Withholding is applied on the gross sales price of the U.S. real estate.

Summary of Section 899

Section 899, if enacted, would significantly increase the U.S. tax cost for foreign persons from countries identified by Treasury as imposing unfair foreign taxes. The retaliatory measures include escalating tax rate increases, override of treaty benefits, and expanded application of the BEAT. The provision is designed both as a revenue raiser and as leverage in international tax negotiations, but it carries the risk of deterring inbound investment and increasing the complexity of cross-border tax compliance.

Additional International Tax Changes

The Global Intangible Low-Taxed Income (GILTI) – GILTI taxes the income of foreign subsidiaries of U.S. persons. Income included under GILTI by Corporations is allowed a 250 Deduction, effectively taxing foreign inclusions at a reduced income tax rate. The House bill proposal reverses the scheduled decrease in the deduction, replacing it with a permanent deduction of 49.2%.

Foreign-Derived Intangible Income (FDII) – FDII provides an export incentive for corporations exporting goods, services or intangibles into foreign markets for foreign use. Similar to GILTI, FDII provides a 250 deduction to reduce the effective tax rate on income from foreign exports. The House bill proposal reverses the scheduled decrease in the deduction, replacing it with a permanent deduction of 36.5%.

Base Erosion and Anti-Abuse Tax (BEAT) – BEAT is a minimum tax for entities with revenues exceeding $500 million. This adjusted taxable income base is applicable to companies with deductions of payments to foreign related entities in excess of 3% of its total deductions. Special rules exist related to the modifications to both deductible expenses and applicable tax credits. The House bill proposal reverses the scheduled tax increase; however, an increased tax rate would still apply to companies impacted by Section 899 discussed above.

Subpart F – U.S. Shareholders may also be subject to income inclusion of certain types of foreign subsidiary income under Subpart F, subject to various exceptions. Noticeably absent in the House bill is the §954(c)(6) extender “Look-Through” exception that has been extended annually since 2009. This provision allows payments made between foreign subsidiaries to be exempt from Subpart F inclusion in a U.S. Shareholder’s taxable income. In the case that the Look-Through exception extender is not included in the final bill, shareholders of multiple foreign subsidiaries will need to analyze any potential impact to their taxable income with the expiration of this exception.

We expect that further amendments to these international provisions will continue as the Senate continues to debate and negotiate the final tax bill before it is signed by the President.

RKL’s International Tax team stands ready to help you navigate the evolving tax planning and compliance landscape. Stay in-the-know and subscribe to our Insights for What’s Next e-newsletter and check out our Insights and Events pages for related content.